INSCOIN

Insurance INSCOIN is one of the oldest industries, and can be seen as part of the growth of modern business that comes to define the world-wide society.

While the insurance in the form we will recognize today begins with the first insurance contract in 1347, methods for transferring and distributing risks in the monetary economy were observed in China in the third millennium BC. One thing that has dictated the insurance sector for thousands of years is its ability to adapt its practices to adapt to changing technological landscape. From contracts written on parchment for websites and large data, the industry is rapidly changing.

The chain is the latest technological game changer to enter the picture, and many of them predict that distributed books can have profound consequences on the way that insurance companies can work. One important issue is that the technology of the chain seems to be the tailor for the solution is the fundamental principle of "utmost conscientiousness" in insurance contracts. This principle states that each party that enters into an insurance contract has a legal obligation to act with a standard of "honesty exceeding what is normally required in most commercial contracts." This means that the insurer must trust that they are telling the truth to the person who wants to take out insurance. This is different from other contracts, which are usually based on the "Let the Buyer Beware" principle, or the idea that the buyer assumes the risk that the product may not meet its expectations.

Applying a chain of blocks to this question would mean that both the insurance contract and the consumer's personal data can be stored in a distributed book, while the consumer controls access to it. Data is stored on the user's personal device, which can eliminate the need for brokers and other intermediaries who have become intermediaries between insurers and consumers. Not only does the chain offer a promise of reducing costs and efficiency, but it can also help increase revenue, as insurers attract new business through better service.

The "chain" technology can help the wholesale insurance sector to more effectively fulfill its role in supporting the global economy. INSCOIN Just as chains are pursued as a force for positive change in other areas of society - from identifying refugees to better public services - it can also help wholesale insurance perform its duties for the common good.

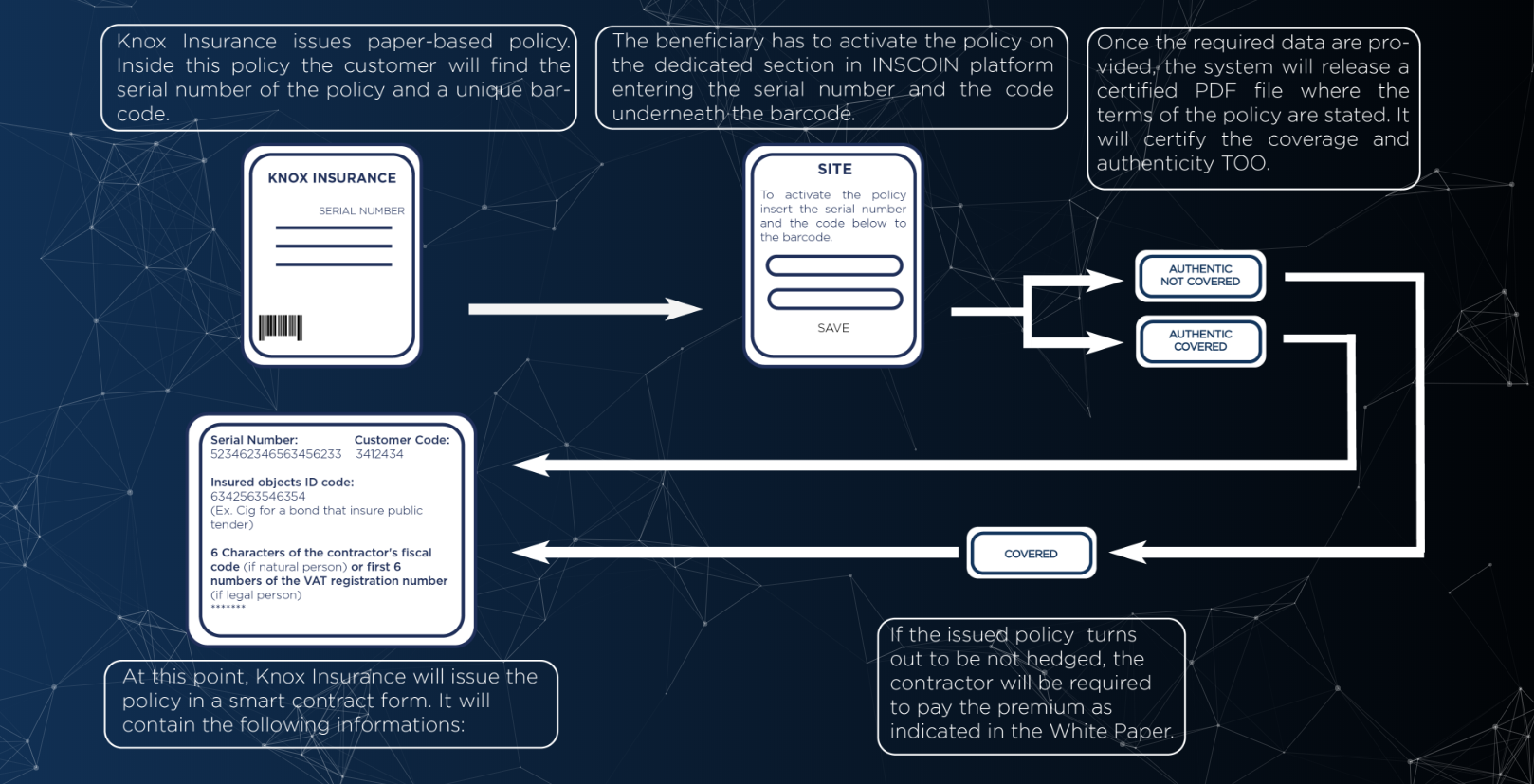

The KNOX project will be the first insurance company that unites the real world with the digital using chain technology, creating the most effective and advanced structure in the sector to find a solution to the problem of certification and anti-forgery of insurance policies. With a smart contract, spreading false insurance policies is avoided, because it is the same system that issues them after receiving payment. With a smart contract, the company will not have a delay in collecting loans, since the policy is issued only after receiving the payment. This factor is aimed at a significant improvement in the management of the company itself. With a smart contract in the event of an accident, a real judge who will decide whether to pay them is no longer a company that can have opportunistic behavior, but the chain system that, in a completely disinterested person's opinion, will decide if this accident is in line with the policy provisions. This advantage will be the most important, as this will increase the transparency of the company in relation to customers.

With a smart contract, spreading false insurance policies is avoided, because it is the same system that issues them after receiving payment. With a smart contract, the company will not have a delay in collecting loans, since the policy is issued only after receiving the payment. This factor is aimed at a significant improvement in the management of the company itself.

INSCOIN With a smart contract in the event of an accident, a real judge who will decide whether it is worth paying them is no longer a company that can have opportunistic behavior, but the chain system that, in a completely disinterested opinion of the individual, will decide if this accident is in line with the policy provisions. This advantage will be the most important, as this will increase the transparency of the company in relation to customers.

Information on the token:

Ticker: INSC

Type: erc20

Total delivery: 500 '000' 000 INSC

Tokens for sale: 270 '000' 000 ISNC

Exchange rate: 1 higher school = 5'000 INSC

Soft cap: 4 '000

Hard cover: 39 '444

Undistributed markers will be burned after the end of the ICO.

Pre-ICO begins: June 23, 2018

Pre-ICO ends: July 7, 2018

pre-sale price: 1 INSC = 0.0002

ICO Price: 1 INSC = 0.0002

Acceptance: high school

Soft cover: 4000

Hard cover: 39444

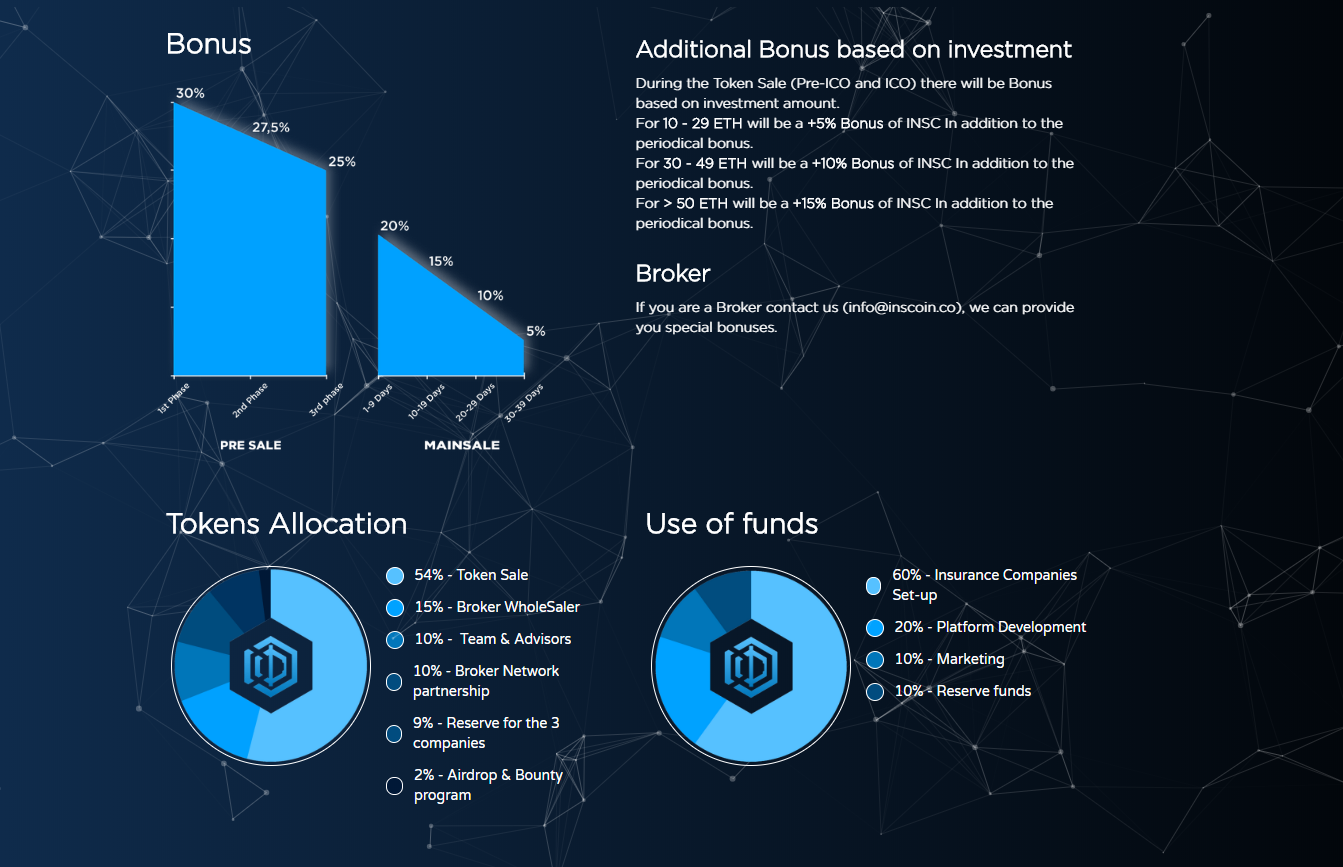

Bonus: up to 30%

ICO begins: July 23, 2018

ICO Ends: August 23, 2018

Detailed information:

Website: https://www.inscoin.co

White Paper: https://inscoin.co/Assets/Content/whitepaper_en.PDF

Twitter: https://Twitter.com/inscoinforknox

Reddit: https://www.Reddit.com/r/InsCoin

Telegram: https://t.Me/inscoinico

Username: Joseph cristian

My Ethereum address: 0x8f0A94f868871EE4ccd00AFaAe3AcB3f0c2A27aA

Komentar

Posting Komentar